Many have written about the millennial generation and whether or not they, as a whole, believe in homeownership as part of attaining the American Dream.

Millennials have taken longer to obtain traditional milestones than the generations before them, such as getting married, having kids, and buying a home. However, that does not mean that they do not still aspire to achieve those things.

History shows that people tend to buy their first home around age 30. Nearly 5 million millennials will turn 30 in the next two years. This will continue to fuel demand for housing.

This is also one of the many reasons why the millennial homeownership rate has continued to grow over the past few years. 48.4% of Americans between the ages of 30-34 now own a home.

There are over 46 million millennials (33% of the generation) who are considered “Mortgage Ready”,meaning they meet the qualifications to be approved for a mortgage today!

a FICO Score ≥ 620

a Back-End Debt to Income Ratio ≤ 25%

no Foreclosures or Bankruptcies in the last 7 years

no severe delinquencies in 1 year

Rob Chrane, CEO of Down Payment Resource, commented on the findings of the report,

“We now know there are millions of buyers with the income & credit necessary to qualify to buy a home. The biggest question is:

Do they know it? …Unfortunately, many renters don’t investigate homeownership simply because they don’t believe it’s an option.”

The good news is that more and more millennials are realizing that they can afford a home now. Even so, more can be done to increase awareness of low down payment programs to attract even more of this generation.

New data from realtor.com shows that in December, millennials accounted for 42% of all new home loans originated in the month. This is more than any other generation.

Bottom Line

If you are one of the many millennials who may be “Mortgage Ready” but are unsure what your next steps should be, contact me (or a local real estate professional) who can help guide you on your path to homeownership.

Home buyer, beware! The seller may be watching. And listening.

A growing number of home sellers are using security cameras and microphones to spy on potential buyers as they tour their houses or condos. They then may use what they hear or see as leverage in price negotiations.

The trend has been fueled by the spread over the past five years of inexpensive Wi-Fi enabled cameras and mics that homeowners can buy and set up themselves for home security. Motion sensors notify them by text or email that a visitor is in their house, and they can then observe a prospective buyer on a computer, laptop or smartphone through the Internet. Alternatively, they can view a recording later.

“Recording devices are cheaper and more readily available,” says Leslie Walker, deputy general counsel of the National Association of Realtors.

Last October, a retired civil service worker bought a three-bedroom house in Richmond Hill, Ga., for about $250,000, says Andi DeFelice, who represented the buyer as a broker at Exclusive Buyer’s Realty. After the retiree moved in, his next-door neighbor told him the seller “’knew he had a buyer the minute you walked through,’” DeFelice recounted.

He was right. When DeFelice and her client toured the home, they both gushed that it was perfect for his need for an isolated workshop to tinker with computers and TVs. The property came with a detached small building with a kitchen, bathroom, living area and two-car garage.

DeFelice believes the intelligence the seller had didn’t affect the bargaining. The retiree paid $15,000 less than the asking price. But “it’s not a comfortable feeling to know that you’re being recorded,” says DeFelice, whose agency represents buyers only and who heads the National Association of Exclusive Buyer Agents. “I was annoyed because my client was annoyed.”

Now, she says, she routinely tells potential buyers to curb their enthusiasm while they’re in the house. “Before we walk in the door, I say, ‘Pretend the seller is home’ or ‘Pretend somebody is listening.’ Because you never know.

In a survey conducted by Harris Poll for NerdWallet this month, 15% of Americans who have ever sold a home said they’ve use surveillance cameras to monitor potential home buyers. And 67% say they would use such cameras if they were selling a home that already had them.

“In a competitive housing market, everything is fair game,” says Holden Lewis, a housing analyst for NerdWallet, a personal finance website.

About 9.4 million U.S. homes, or 7.4% of the total, are equipped with Wi-Fi enabled cameras and mics, says Brad Russell, research director for Parks Associates, a consumer technology research firm. As many as 11 million or so have similar but more limited set-ups trained on the doorstep or outside the house, or embedded in a light fixture, Russell says. That means up to 13% of homes have at least one Wi-Fi camera and mic. The cameras often are visible but can be hidden in stuffed animals, like a “nanny cam,” or concealed in bookshelves. This Web-enabled do-it-yourself home surveillance market didn’t even exist five years ago, Russell says.

By 2022, as many as 50 million homes are projected to have at least one Wi-Fi camera, Parks forecasts. An average camera and mic costs $122, Russell says.

Spying may be illegal

Yet snooping home sellers may be breaking the law.

Surveillance laws vary by state. Video monitoring is generally prohibited in places where someone has “a reasonable expectation of privacy,” according to a summary of state laws compiled by the National Association of Realtors (NAR). Such privacy zones likely would not include other people’s homes. In many states, however, eavesdropping or recording audio requires the consent of at least one person being recorded, and some require the sign-off of all the parties.

In other words, audio recording likely would be legal in many states if the home seller is accompanying the buyer. But not in the more common scenario in which the only ones monitored are the house hunter and his or her broker, both unsuspecting.

Sellers “need to disclose it, put a sign up or turn it off,” says Lou Nimkoff, a broker at Brio Real Estate in Winter Park, Fla., and president of the Orlando Regional Realtors Association.

NAR recommends that listing brokers ask home sellers if they’re using surveillance equipment, Walker says. If so, they should tell the buyer’s agent or include a notice in the home listing that all brokers can see, she says. Some regional Realtors’ groups now require home sellers to inform their brokers of any surveillance equipment as part of standard broker contracts, Walker says.

Shhh! Don’t say you like the house!

Gea Elika, a New York City broker, estimates that up to a third of the condominiums he shows have surveillance equipment because most of them cost at least several million dollars. A few years ago, a client saw a camera move as she toured a condo.

“She kind of wanted to get out of there,” says Elika, principal broker at Elika Associates. “She thought it was creepy” and didn’t buy the unit.

Victoria Henderson, a broker at Buyer’s Edge in Bethesda, Md., says she noticed a green light flash on a camera as she showed a young couple a four-bedroom house in Ellicott City about a week ago. She immediately told them, “Don’t say anything like, ‘I love this house.’ ” Now, she says, she also steers clear of criticizing features of a home while in it for fear of offending the owners.

Many home sellers and their brokers have a different perspective. A couple of years ago, sellers in Atlanta used a nanny cam to record what prospective buyers said because they wanted to know what they didn’t like about the house, says their agent, Jen Engel of Keller Knapp. The house had been languishing on the market.

“In my opinion, if you’re not comfortable with (home surveillance), that’s your problem and not mine,” says Engel, who has security cameras in her own house and believes buyers should always assume they’re being recorded. “It’s my house, and I can do it if I want to.”

Kristen’s comments: I, 100%, Vehemently DISAGREE WITH JEN ENGEL, above.

In North and South Carolina, video taping IS legal- but Audio taping is NOT Legal- this law varies per state.

To use security cameras to video tape people as they walk through your home is understandable- you want to make sure strangers are not going through your valuables (although with a licensed and bonded Realtor at their side, that is highly unlikely- in fact, I have never witnessed this in my 27 years of practicing real estate). Open Houses are another story, however, as sellers are vulnerable when they open their doors to everybody and their brother; ie, people that they do not know. Stories have been reported of vandals using Open Houses to steal seller’s valuables, or to ‘case the house’ to come back for a break in later (although this is, thankfully, a rare occurrence). I always tell my Agents to have at least one other person (another Agent or a trusted friend or spouse) to go with them when they hold Open Houses, so when the Agent is downstairs with one prospective buyer, someone else can be upstairs with the rest of the horde touring through the home, as one Agent cannot be in two places at once. This is also important for the Agent’s safety, so they don’t get trapped in a room (that’s a whole other post, folks)!

So, why is Audio taping illegal? Let’s think about this for a minute. Is it really fair and ethical to snoop and eavesdrop on what is supposed to be a client / Broker privileged conversation, with the express intention of gaining the upper hand in the negotiation of your home? Here again, one should go by the ‘Golden Rule”- think back to the times when you were looking at homes, and all of the comments you, or you and your wife or husband, made, while walking through. Whether negative, “Oh my gosh, that wallpaper! That carpet! Disgusting! What century is this couple living in”? Or, if you are super excited because, after what seems like hundreds of homes, you finally found THE one- “I LOVE, LOVE, LOVE THIS HOUSE! Do you think that they will throw in the ‘fridge? How much do you think we should offer for it? Do you think we have to go full price to get it, or can we ask for closing costs”?

To try to gain an unfair advantage is, to me, unethical. If you wouldn’t want that done to you, then you shouldn’t be doing it to others. And ask yourself, is your moral compass so weak that you can’t discern the difference between saving a few bucks and screwing the person that in good faith, is bringing you a home sale? Really, folks, this is a no-brainer.

I had this happen about a year and a half ago, when my buyers and I were walking through a home- it was when those baby eaglets were born and nesting, I remember that very clearly, because there was an open laptop left running, smack dab in the middle of the living room. I thought that was very odd, that the sellers hadn’t been advised to put away their valuables prior to showings (which they knew well in advance about, as I try to schedule my appointment at least a day in advance, if possible, for consideration to the sellers, who have to make arrangements to leave the home for showings). Of course, the buyers were all giddy, and we talked about potential offer scenarios, discussed asking the seller to leave certain items like the kitchen table “it’s so perfect here! We would like them to leave it. We really, really love this table, and it fits so perfectly. We won’t want to kill the deal over it, so if they don’t want to leave it, it’s no big deal, but we want to ask for this and the garage shelving, anyway”.

I go back to the office, and pull the comps, flood maps, tax records, past deeds and title, etc.- all of the due diligence stuff that we Brokers do, to make sure that our offer is sound and there are no ‘red flags’ upon discovery, that would disqualify this house (major road coming behind or nearby the house, home was built in a flood plain and would require expensive flood insurance, etc.). We schedule a return appointment to walk through a second time (a second showing is always a good sign of a potential incoming offer).

Two days later, there is a sign in the window, stating that “This home is under video and audio surveillance”. Ah so THAT is what the laptop and “baby eaglets” was all about. GRRRREAT, we find this out now, after we’ve already been surveilled! How do you think that made the buyers (and me!) feel? I was so angry at the sellers trying to ‘dupe’ my unsuspecting buyers, if I could have found them another home that they liked equally well, I would have! I called the other Broker and explained the situation, and his response was, “it’s their home. They can do whatever they want”. Ummm, NO, they can’t. I explained that they were within their rights to video tape, but the law in North Carolina was clear, that it is illegal to audio tape people without their consent, and it was his responsibility to be clear to these sellers going forward about the laws. His response? “Not gonna’ happen”. I made sure to include that in my feedback to the sellers, to be sure, but the damage was already done. We ended up closing on that home, but the process was onerous, with very difficult sellers, and a lazy, indifferent Agent. Once the buyers moved in, the entire street came over to “thank them” for buying the home. All of the other homeowners on the street rally hated these people, and were hopping about with joy to see them pack and move. They even told the buyers that ‘they were praying that nothing happened to make the deal fall through”, so “The Nasties” would be out of their neighborhood, for good. All I could say to my buyers was that, “Karma is a b*tch”!

What do y’all think about audio and video surveillance? Weigh in, below!

If you are buying or selling a home, NEVER forget to CALL THE CLOSING ATTORNEY (OR GO IN PERSONALLY) TO GET WIRE INSTRUCTIONS. DO NOT RELY ON AN EMAIL FROM ANYONE (The Attorney, your Realtor, your lender). I have shared this before, and it is scary stuff. This is becoming more prevalent, and it even happened to one Charlotte couple recently. Please share with anyone thinking about buying or selling a home! This IS happening, folks!

Provided as an excerpt from an article written by KrebsOnSecurity on April 17, 2017

Blind Trust in Email Could Cost You Your Home

The process of buying or selling a home can be extremely stressful and complex, but imagine the stress that would boil up if — at settlement — your money was wired to scammers in another country instead of to the settlement firm or escrow company. Here’s the story about a phishing email that cost a couple their home and left them scrambling for months to recover hundreds of thousands in cash that went missing.

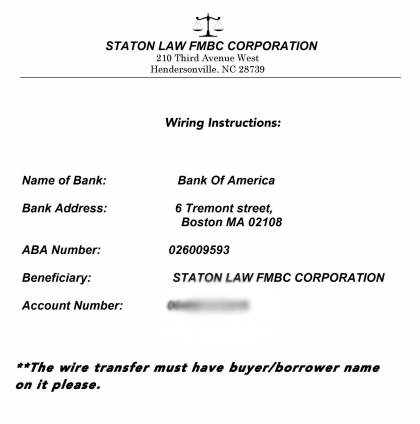

It was late November 2016, and Jon and Dorothy Little were all set to close on a $200,000 home in Hendersonville, North Carolina. Just prior to the closing date on Dec. 2 their realtor sent an email to the Little’s and to the law firm handling the closing, asking the settlement firm for instructions on wiring the money to an escrow account.

An attorney with the closing firm responded with wiring instructions as requested, attaching a document that had the law firm’s logo and some bank account information that was represented as the seller’s account number. The Little’s realtor sent the wire on Thursday morning, the day before settlement.

“We went to closing at 1 p.m. on Friday, and after we signed all the papers, we asked the lawyers if we were going to get back the extra money we had sent them, because they hadn’t be able to give us an exact amount in the wiring instructions. At that point they told us they had never gotten the money.”

After some disagreement, both legitimate parties to the transaction agreed that someone’s email had been hacked by the fraudsters, and was used to divert the wired funds to an account the criminals controlled. The hackers had forged a copy of the law firm’s letterhead, and beneath it placed their own Bank of America account information (see screen shot above).

The owner of the Bank of America account appears to have been a willing or unwitting accomplice — also know as a “money mule” — recruited through work-at-home job schemes to receive and forward funds stolen from hacked business accounts. In this case, the money mule wired all but 10 percent of the money (a typical money mule commission) to an account at TD Bank.

Fortunately for the Littles, the FBI succeeded in having the resulting $180,000 wire transfer frozen once it hit the TD Bank account. However, efforts to recover the stolen funds were stymied immediately when the Littles’ credit union refused to give Bank of America a so-called “hold harmless” agreement that the bigger bank wanted as a legal guarantee before agreeing to help.

Charisse Castagnoli, an adjunct professor of law at the John Marshall Law School, said banks have a fiduciary duty to their customers to honor their requests in good faith, and as such they tend to be very nervous legally about colluding with another bank to reverse payment instructions by one of their own customers. The “hold harmless” agreement is usually sought by the bank which received a fraudulent wire transfer, Castagnoli said, and it requires the responding bank to assume any and all liability for costs that the requesting bank may later incur should the owner of account which received the fraudulent wire decide to dispute the payment reversal.

“When it comes to wire fraud cases the banks have to move very quickly because once the wires make it outside the U.S. to foreign banks, the money is usually as good as gone,” Castagnoli said. “The receiver or transferee usually insists on a hold harmless agreement because they’re moving the money on behalf of their own account holder, kind of going against their own client which is a big ‘no-no’ when you’re a fiduciary.”

But in this case, the credit union in which the Littles had invested virtually all of their money for more than 40 years decided it could not in good faith provide that hold harmless agreement, because doing so would stipulate that the credit union affirms the victim (the Littles) hadn’t willingly and knowing initiated the wire, when in fact they had.

“I talked to the wire dept multiple times,” Mr. Little said of the folks at his financial institution, Atlanta, Ga.-based Delta Community Credit Union (DCCU). “They finally put me through to the vice president of loss prevention at the credit union. I’m not sure they even believed all that was going on. They finally came back and told me they couldn’t do it. Their rules would not allow them to send a hold harmless letter because I had asked them to do something and they had done it. They had a big meeting last week with apparently the CEO of the credit union and several other people. Then they called me on Monday again and told me they would not could not do it.”

The Littles had to cancel the contract on the house they were prepared to occupy in December. Most of their cash was tied up in this account that the banks were haggling over, and so they opted to get a heavily mortgaged small townhome instead, with the intention of paying off the mortgage when their stolen funds are returned.

“We canceled the contract on the house because the sellers really needed to sell it,” Jon Little said.

The DCCU has yet to respond to my requests for comment. But less than a day after KrebsOnSecurity reached out to the credit union for comment about the Littles’ story, the bank informed the Littles that the other bank would soon have its hold harmless letter — freeing up their $180,000 after more than four months in legal limbo.

The Littles’ story has a fairly happy ending, however most of the other few dozens stories previously featured on this blog about wayward mortgage, escrow and payroll payments wound up with the victim losing six figures at least.

One of the more recent advertisers on this blog — Ninjio — specializes in developing custom, “gamified” security awareness training videos for clients. “The Homeless Homebuyer,” one of the videos Ninjio produced for a government client seems appropriate here: It features an animated FBI agent breaking the bad news to some would-be homeowners that their money is gone and so are their dreams of a new home — all because everyone blindly trusted unsecured email for what is essentially a high-risk cash transaction.

I like the video because its message is fairly stark and real: You could get screwed if you don’t take this seriously and proceed carefully, because once the money’s gone it usually stays gone. Check it out here:

So here’s what you need to know if you or anyone you know, love or even like are about to buy or sell a home: Never wire money based on the say-so of one party to the transaction made via email. You simply don’t know if their account is hacked, so from a self-preservation standpoint it’s best to assume it is.

Agree in advance who will contact whom — preferably by phone — on settlement day to receive the wiring details, and who will manage the wiring process. Never trust bank account details and payment instructions sent via email. Always double or even triple check any instructions for wiring money at settlement. Confirm all wiring instructions in person if possible, or else over the phone.

By the way, these same precautions can help make organizations less susceptible to CEO fraud schemes, email scams in which the attacker spoofs the boss and tricks an employee at the organization into wiring funds to the fraudster.

The Federal Bureau of Investigation (FBI) has been keeping a running tally of the financial devastation visited on companies via CEO fraud scams. In June 2016, the FBI estimated that crooks had stolen nearly $3.1 billion from more than 22,000 victims of these wire fraud schemes.

Castagnoli said many credit unions and small banks don’t have the legal staff with the clearance to make calls on whether to issue a hold harmless agreement, and so they usually try to punt on that when requested. Were she in The Littles’ position, Castagnoli said she would have called the head of the credit union and demanded assistance.

“If the head of the bank wouldn’t do it, I’d call my congressperson or a state banking regulator,” she said.

![Kristen Haynes Five Star 2018 REVISED[567]](https://charlotterealtypros.wordpress.com/wp-content/uploads/2018/03/kristen-haynes-five-star-2018-revised567.png?w=345&h=199)